Management Discussion and Analysis

(extracted from Annual Report 2024)

BUSINESS OVERVIEW

Our Group's humble beginning can be traced back to 1993 when HongPeng Footwear was founded in Jinjiang City, Fujian Province, China to carry out manufacturing of sports shoes. Our Group promptly recognised that it is important to create a proprietary brand to help differentiate ourselves from other industry players, and to move up the value chain. Accordingly, our Group's proprietary brand name - 'XiDeLang' was created.

To facilitate the management process, HongPeng Fujian was established in 1996 to focus on design, manufacturing and marketing of sports shoes as well as design and marketing of sports apparel, accessories and equipment under 'XiDeLang' brand ("Own-Branding Segment"); whilst HongPeng Footwear concentrates on manufacturing of sports shoes for external customers where the products are primarily for distribution in overseas markets ("ODM Segment").

In view of the intensified market challenges and adverse impact of COVID on the operations of the authorised distributors, our Group has resolved to cease the operations of Own-Branding Segment during the financial year ended 30 June 2022. To optimise the production efficiency following the cessation of Own-Branding Segment, the manufacturing activities of ODM Segment have been transferred and consolidated into HongPeng Fujian.

During the financial period from 1 July 2023 to 31 December 2024 ("financial period under review" or "FPE 2024"), there is no change in the principal activities of our Group, where our Group's business operations continue to focus on ODM Segment.

ODM Segment

-

Objective:

To become the reliable, trusted production partner for international brand names.

-

Targeted Customer:

International brand names, where products are primarily for distribution in overseas markets.

-

Distribution Channel:

Foreign trading / export companies and intermediaries based in China.

-

Focus and business strategies:

-

Production and design capability and capacity

Our Group has continued to build on the production capability and capacity throughout the years. Relocation to our Group's present headquarters and production centre (with a builtup area of over 110,000 square meters) in 2013 has enabled us to expand our production capacity and to centralise the sports shoes manufacturing operations at single location, thereby allowing us greater flexibility and efficiency in accommodating the changes in market demands.

The relocation to our Group's present headquarters and production centre, which comes with wider production floor, has enabled us to install additional production lines to enhance our production and design capability as well as to expand our production capacity.

The enhanced production and design capability and increased production capacity are part of the key components which our Group leverages on, to secure new ODM production orders and enhance customers' confidence for recurring orders.

To optimise the production efficiency following the cessation of Own-Branding Segment, the manufacturing activities of ODM Segment have been transferred and consolidated into HongPeng Fujian.

-

Supply-chain management and quality control

Our Group practices stringent checks and controls to uphold our quality commitment to the ODM customers. Raw materials to be used for the production are inspected to ensure adherence to the agreed specifications. Checks and controls are carried out at various stages of the production to ensure prompt detection of any defects and deviations from the agreed specifications. Finished products must undergo various testing and inspection for quality assurance prior to delivery.

Over the years, we have strengthened our in-house research and product development team. This enables us better integration and control for the entire production flow, as all key aspects (conceptual design, raw material procurement, costing, production process and production time) are considered and ascertained early at design stage.

Our Group maintains a close relationship with the raw material suppliers to ensure that the incoming supplies are of good quality with prompt delivery. All the supplies are sourced domestically, with majority of the suppliers located within the neighbouring areas. The proximity allows us better communication with our suppliers, where any issues concerning the supplies can be resolved expediently.

-

PERFORMANCE REVIEW

No comparative figures are available for presentation. The Board of Directors have approved the change of financial year end from 30 June to 31 December. The audited financial statements as disclosed in this Annual Report are for financial period from 1 July 2023 to 31 December 2024, covering a period of 18 months. Thereafter, the subsequent financial year shall end on 31 December annually. The change is to synchronise the financial reporting period with the calendar year, permitting thorough sale recording and operational planning, hence improving decision-making processes. Kindly refer to the Company's announcement made on 23 April 2024 for further details.

Revenue and Profitability

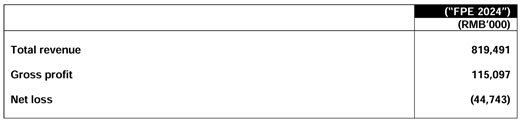

Our Group recorded total revenue of approximately RMB819.5 million and gross profit of approximately RMB115.1 million for the FPE 2024, derived from sales of footwear from the ODM Segment.

Our Group recorded net loss of approximately RMB44.7 million for the FPE 2024, mainly due to administrative expenses incurred of RMB153.2 million, which were primarily attributable to the following items:

-

research and development expenses incurred for the research on suitable new raw materials, in line with our Group's strategy to keep abreast of the industry development and to sustain competitiveness;

-

staff costs for management, administrative and support functions; and

-

compensation/rebate to customer for late delivery of orders.

Financial Position

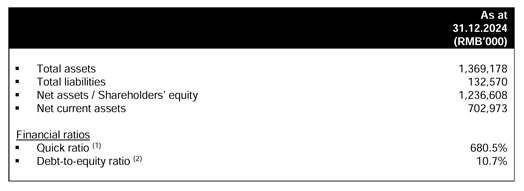

(1) Formula: (Cash and cash equivalents + Receivables) / Current liabilities

(2) Formula: Total liabilities / Shareholders' equity

Our Group's financial position as of 31 December 2024 remained relatively healthy and stable.

Liquidity

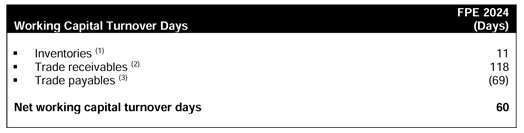

(1) Formula: Inventories / Cost of sales x 549 days

(2) Formula: Trade receivables / Revenue x 549 days

(3) Formula: Trade payables / Cost of sales x 549 days

Our Group's net working capital turnover days for the FPE 2024 stood at 60 days.

Capital Requirements, Structure & Resources

As of 31 December 2024, our Group had sufficient cash reserves to fund the existing capital expenditure requirements, to settle the existing indebtedness and to carry out our day-to-day business operations. Although there is no immediate shortage in capital resources, our Group may, from time to time, assess the need for additional fund-raising to meet future capital expenditure requirements while ensuring that our Group's financial and liquidity position remains healthy.

Dividend Policy

The Board has established a dividend policy to distribute up to 20% of the Company's profit after tax as dividend payment to our shareholders. The dividend payment will be made after taking into consideration, inter alia, cash availability, return on equity and the projected level of capital expenditures; always bearing in mind the importance of long-term value creation for our shareholders. The declaration of interim dividends and the recommendation of any final dividends are subject to the discretion of the Board, whilst any final dividend proposed is subject to our shareholders' approval.

In view of the economic uncertainties and the prevailing market challenges, no dividend was proposed by our Group during the FPE 2024 to preserve liquidity. This will give our Group's better positioning in handling future challenges and to tap into new opportunities.

TREND & RISK FACTORS

Known Trend

The key factor/trend affecting our Group's performance for the recent years, as well as the financial period under review, is the intensifying market competition for the footwear and apparels market; which was further complicated due to the economic uncertainties and geopolitical tensions. Our Group had taken the following initiatives to mitigate the impact arising from the intensifying market competition:

-

Stepped up the efforts in securing additional ODM production orders, to diversify the revenue base of our Group;

-

Enhanced the sports shoes production capability and capacity of the Group, so that our Group is more flexible in accommodating to the changes in market demands; and

-

Adopted prudent cost control initiatives as well as introduced suitable initiatives to promote customer loyalty and long-term business relationship.

Principal Risk Factors

The principal risk factors faced by our Group's operations remained largely consistent with prior years, comprising the following:

Kindly refer to Statement on Risk Management and Internal Control contained in this Annual Report for further details on the key risk management processes that have been put in place by our Group to mitigate the impact of the abovementioned principal risk factors.

PROSPECTS

Looking ahead to 2025, the increasing unpredictability of global economic conditions, coupled with geopolitical tensions, may continue to pose challenges. Consumers worldwide are expected to remain cautious in their spending, while competition within the industry continues to intensify. Despite these uncertainties, the sportswear market is showing signs of recovery, though subject to evolving market dynamics.

Our Group remains vigilant in managing operational costs while proactively exploring expansion opportunities, both within China and internationally. Overseas expansion offers strategic advantages, including diversification of revenue streams, access to new markets, and enhanced resilience against domestic market fluctuations. In the post-pandemic era, we are committed to prudent operational strategies, continuously optimizing management efficiencies while actively seeking avenues for sustainable growth. Through disciplined cost control and well-calibrated expansion measures, we aim to strengthen our competitive position and establish a robust foundation for long-term stability and development.

As part of our international expansion efforts, the Company has identified Indonesia as a promising market and is currently evaluating a potential joint venture in the country. Following extensive market surveys and discussions initiated in late 2023, the Company, together with its prospective partner, Mr. Xia ZiXuan, has taken preliminary steps towards establishing a shoe manufacturing presence in Indonesia. To facilitate initial groundwork, PT NBF Shoes and Clothing was incorporated on 1 November 2023, with the Company's Director of Business Development and Foreign Investment, Mr. Ding WeiBin, serving as its legal representative.

At present, the investment in Indonesia remains under review, with key partnership terms and operational strategies still under discussion. The total investment commitment, funding structure, and governance framework have yet to be finalised. A detailed announcement will be made once the Company reaches a conclusive decision on the investment and its execution.

The Company remains committed to transparency and will provide further updates on this initiative as and when appropriate.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains certain forward-looking statements with respect to the financial condition, results of operations and business of our Group. Wordings such as "expects", "estimates", "anticipates", "intends", "plans", "believes", "potential", and variations of these wordings and similar expressions are intended to identify forward-looking statements. These forward-looking statements represent our Group's expectations or beliefs concerning future events and involve inherent risks and uncertainties. Forward-looking statements speak only as of the date they are made, and one should not assume that they have been revised or updated in the light of new information or future events. Accordingly, undue reliance should not be placed on them. Readers should be cautioned that several factors could cause actual results to differ, in some instances materially, from those anticipated or implied in any forward-looking statement. Trends and factors that are expected to affect our Group's results of operations are disclosed in the above sections.